For many adults managing households, financial stress does not start with debt, unemployment, or a sudden crisis. Often, it begins quietly — with silence.

Before we intentionally started communicating about money, our financial life seemed stable. Bills were paid on time. We maintained some savings. We did not argue about money. Neither of us thought it was a source of conflict.

Yet, stability without clarity is fragile.

Our financial habits operated in parallel rather than in partnership:

One of us focused on long-term investing.

The other prioritized liquidity and flexibility.

We assumed our views were aligned. They were not.

The turning point came when an unexpected medical expense forced us to decide quickly how to respond. While we had the resources to cover the cost, the discussion about how to use them revealed tensions we hadn’t noticed.

That moment taught us a crucial lesson:

Financial preparedness does not guarantee financial confidence.

Research consistently shows that money is one of the most common stressors in adult relationships. A 2023 Fidelity study found that 45% of couples argue about money at least occasionally, even when income is not the primary issue [1].

The problem was not a lack of discipline or income. It was a lack of shared structure.

Step 1: Identifying Hidden Financial Misalignment

We realized that disagreement is not always loud. Sometimes it is quiet — invisible in daily life.

For instance:

One of us believed retirement contributions should be maximized early to leverage compound growth.

The other believed accessible cash reserves were the real foundation of security.

Neither view was wrong — but we had never explicitly discussed priorities.

When the unexpected expense occurred, this difference surfaced in the form of hesitation:

Should we draw from investments?

Or preserve long-term growth and rely on savings?

The tension was not due to opposing values — it came from undefined ones.

According to OECD research, households with clearly defined financial goals respond more effectively to financial shocks than those operating without shared planning frameworks [2].

We learned that alignment is not automatic. It must be built intentionally.

Step 2: Replacing Casual Conversations with Structured Dialogue

Initially, we tried to “talk more about money.” This failed. Conversations were inconsistent, emotionally influenced, and unfocused.

We introduced a structured monthly review system that included:

2a: Spending Transparency

We listed:

Fixed costs;

Variable spending;

One-time purchases;

Within two months, we discovered grocery spending had increased by 28% — not solely due to inflation, but due to convenience-driven purchases during demanding workweeks.

This was not a failure of discipline; it was a behavioral response to stress.

2b: Emotional Reflection

Instead of judging spending, we asked:

Which purchases reduced stress?

Which created regret?

Patterns emerged:

Online purchases after difficult workdays;

Increased food delivery during fatigue;

The American Psychological Association has linked stress to short-term financial decision-making that prioritizes relief over long-term planning [3]. Recognizing this allowed us to replace blame with understanding.

2c: Forward Planning

We discussed upcoming obligations and trade-offs. For example:

Temporarily reducing discretionary travel to accelerate emergency savings

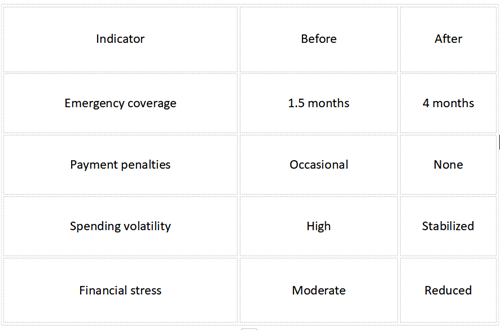

Within six months, our emergency fund grew from covering 1.5 months of expenses to four months.

Step 3: Introducing a Shared Budgeting Framework

We adopted a zero-based budgeting model: every dollar received had a designated purpose:

Spending;

Saving;

Investing;

Buffering;

This clarified intent without restricting flexibility.

World Bank research indicates that structured financial allocation improves household stability across income levels [4].

We felt more in control — not because we spent less, but because we spent consciously.

Step 4: Learning from Mistakes

Our system only improved after failure.

We once missed a credit card payment due to oversight. The penalty increased our interest rate by 6%.

Instead of blaming each other, we redesigned the system:

Automated minimum payments;

Scheduled savings transfers;

Automation removed reliance on memory and mood.

Step 5: Defining Financial Security Together

Security meant different things to each of us:

One prioritized retirement readiness.

The other prioritized liquidity and flexibility.

Rather than compromise on one vision, we built balance:

Continued retirement contributions;

Increased liquid reserves;

Research from the National Endowment for Financial Education shows that shared financial vision improves long-term household planning success [5].

Step 6: Measuring Real Change

Within one year, our improvements were measurable:

Step 7: Psychological Impact

Transparency reduced:

Assumptions;

Financial anxiety;

Decision fatigue

Money became less emotional and more functional.

Step 8: Making the System Sustainable

We avoided complexity. Our process remained:

Monthly review;

Quarterly adjustment;

Annual long-term planning;

This simplicity ensured consistency.

Step 9: Global Relevance

Our approach was not income-dependent. It relied on:

Communication;

Structure;

Behavioral awareness;

OECD and World Bank findings confirm these factors improve resilience across economic contexts [2][4].

Step 10: Transferable Lessons

Key insights:

Alignment must be intentional;

Structure reduces stress;

Automation prevents error;

Transparency builds trust;

Step 11: Establishing Decision Governance

Most couples don’t fail because of daily spending; they fail because decision roles are unclear.

Key questions must be answered:

Who decides?

How do we break deadlocks?

What happens when priorities conflict?

Without governance, alignment is temporary.

The Car Replacement Decision

Eight months into our system, our aging car needed costly repairs — 60% of its market value.

Options:

-Repair

Pros: Lower short-term cost, no new debt

Cons: Ongoing repairs, reliability risk

-Replace

Pros: Long-term reliability, reduced stress

Cons: Large upfront cost, possible financing

Our Governance Rule

We introduced a Primary Stakeholder + Joint Impact Rule:

The partner most affected by daily use had primary recommendation authority.

Decisions impacting long-term savings required joint approval.

We applied the rule:

Daily driver recommended replacement;

We jointly reviewed emergency fund impact, financing options, and long-term cost;

Result: We purchased a modest replacement vehicle while preserving 75% of emergency reserves. The decision felt calm — not contested.

Why Governance Matters

The National Endowment for Financial Education shows that households with clear financial decision roles experience:

Less stress;

Faster agreement;

Greater long-term consistency;

Governance transforms communication into coordination.

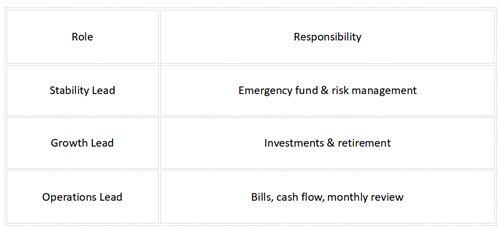

Step 12: Creating Financial Roles

We assigned flexible roles:

This prevented duplicated effort, silent assumptions, and bottlenecks.

Step 13: Handling Disagreements Without Escalation

We implemented one rule: pause major decisions if stress was high.

This avoided reactive spending and defensive behavior. APA research shows stress significantly impacts financial judgment [3].

Step 14: Planning for the Unexpected

We established:

Income interruption plan;

Emergency spending protocol;

Priority hierarchy;

This ensured that alignment survived disruption.

Step 15: Future Alignment

We began annual discussions on:

Career changes;

Relocation possibilities;

Lifestyle priorities;

This connected daily budgeting to long-term life direction.

Step 16: Monthly Review in Practice

A typical monthly review looks like this:

Spending Transparency: Review all transactions, categorize, discuss anomalies

Emotional Reflection: Identify spending driven by stress, reward, or habit

Forward Planning: Adjust upcoming budget based on upcoming events or obligations

For example: Last month, we noticed a spike in dining out. Discussion revealed fatigue-driven convenience. We adjusted by scheduling home-cooked meals and grocery prep.

Step 17: Quarterly Adjustments

Each quarter, we:

Evaluate investment allocations

Adjust discretionary spending goals

Rebalance savings priorities

This keeps short-term habits aligned with long-term strategy.

Step 18: Annual Long-Term Planning

Once per year, we review:

Retirement contribution targets

Emergency fund targets

Major purchases (home, car, travel)

Lifestyle goals (family activities, hobbies)

This ensures we make financial decisions proactively rather than reactively.

Step 19: Integrating Behavioral Insights

We applied research-backed behavioral principles:

Loss aversion: Automating savings reduces the pain of manual transfers

Present bias: Setting short-term milestones keeps motivation high

Stress awareness: Recognizing stress spending prevents emotional overspending

Step 20: Key Takeaways for Any Household

Alignment requires intentional effort, not just avoidance of conflict;

Structured dialogue fosters clarity and trust;

Clear governance prevents deadlocks and hidden resentment;

Automation reduces human error;

Behavioral insight improves decision quality;

Regular review ensures adaptability;

Money becomes a shared system, not an individual burden.

Conclusion

We did not eliminate uncertainty. Instead, we replaced ambiguity with clarity.

Money became a shared strategy, supported by transparency, governance, and behavioral awareness. Financial harmony is not luck — it is intentionally designed.

References:

[1] Fidelity Investments. (2023). Couples & Money Study. https://www.fidelity.com

[2] OECD. (2022). Financial Resilience Framework. https://www.oecd.org

[3] American Psychological Association. (2023). Stress and Financial Behavior. https://www.apa.org

[4] World Bank. (2022). Household Financial Stability. https://www.worldbank.org

[5] National Endowment for Financial Education. (2021). Financial Communication. https://www.nefe.org

About Author:

Daniel R. Hayes is a U.S.-based Certified Financial Planner (CFP) and household finance educator. He specializes in helping adults manage everyday financial decisions through structured dialogue, clear budgeting frameworks, and behavioral strategies. Daniel’s work focuses on helping couples and families align priorities, navigate financial decisions, and create sustainable systems without stress or conflict.

Disclaimer

This article is for educational and informational purposes only and does not constitute financial, legal, or investment advice. Readers should consult qualified financial professionals before making major financial decisions.

Recommend:

The Hidden Costs of Moving Out: What No One Tells You About Independent Living

From Chaos to Order: My Step-by-Step Bedroom Corner Hanging Storage System for Clean Clothes

The Kitchen Seasoning Storage Chaos Resolution Guide: My ‘Common-Backup’ Classification and Positioning Method

My Rational Choice List for Upgrading and Downgrading Consumption